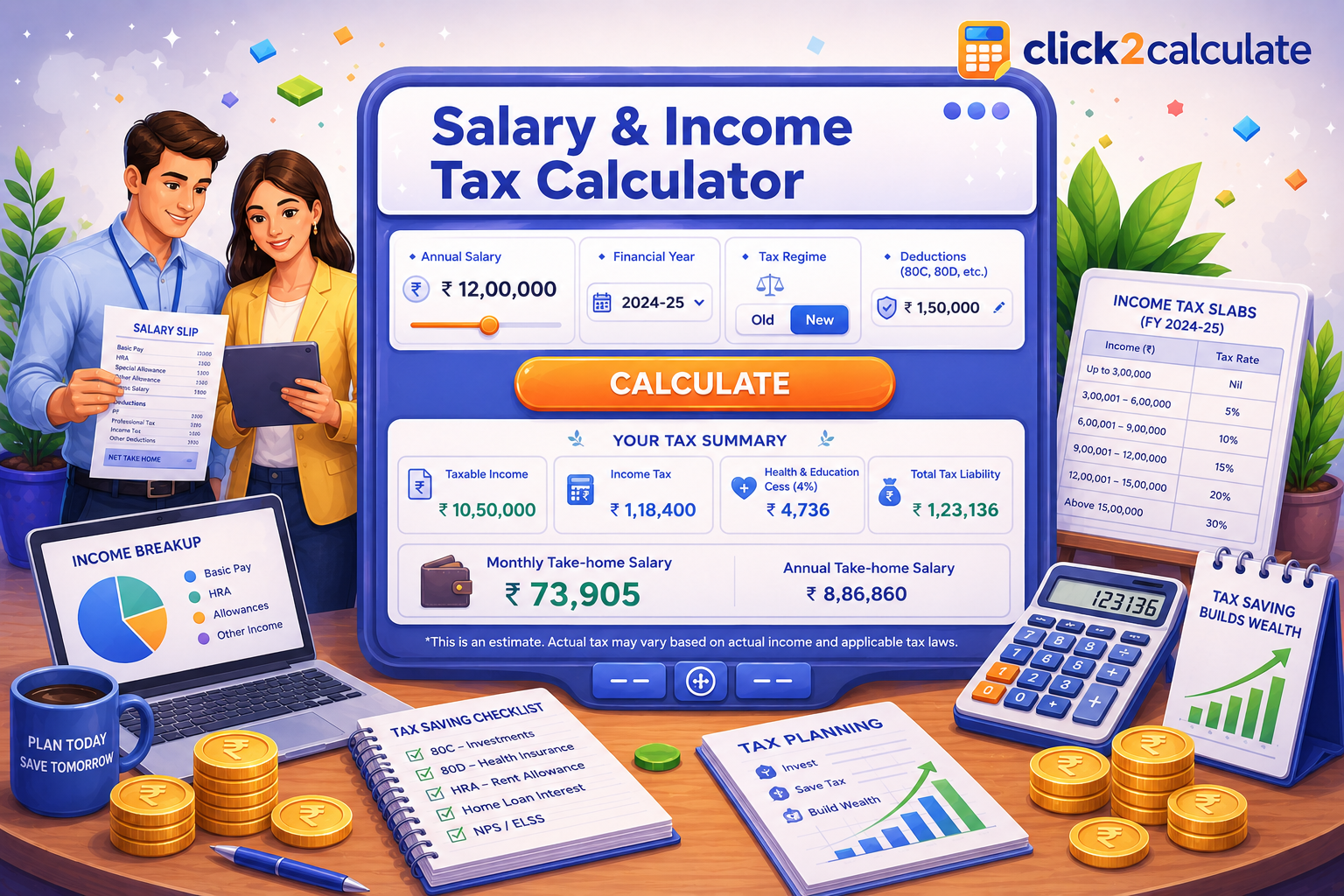

What Is a Salary & Income Tax Calculator? Why You Need One in 2026

A salary and income tax calculator is a free online tool that instantly estimates how much income tax you owe — and more importantly, how much of your salary you actually take home after all deductions, exemptions, and tax liabilities are accounted for.

Whether you are a salaried professional in Bengaluru evaluating a new job offer, an NRI understanding your Indian tax obligations, or a global professional comparing take-home pay across countries before an international move — the Click2Calculate salary income tax calculator gives you accurate, instant, side-by-side results without requiring a Chartered Accountant or complex spreadsheet.

The Click2Calculate tool covers:

- India — New Tax Regime and Old Tax Regime for FY 2025-26 (AY 2026-27), updated for Union Budget 2025

- USA — Federal income tax + Social Security + Medicare (FICA), with state tax options

- United Kingdom — Income Tax + National Insurance contributions for tax year 2025-26

- Australia — ATO income tax + 2% Medicare Levy for FY 2025-26

- Canada — Federal + provincial income tax

- Germany, UAE, Singapore, and more

With Indian income tax rules changing significantly every year, and with the New Tax Regime now the default regime from FY 2023-24 onwards, using an accurate and up-to-date calculator is no longer optional — it is essential for smart financial planning.

India Income Tax Calculator: FY 2025-26 (AY 2026-27) Complete Guide

What Changed in Union Budget 2025 — Key Updates for FY 2025-26

The Union Budget presented in February 2025 introduced several significant changes that every salaried taxpayer must understand before calculating their tax liability:

1. Zero Tax Up to ₹12 Lakh Under New Regime The Section 87A rebate was increased from ₹25,000 to ₹60,000 under the New Tax Regime. This means individuals with total income up to ₹12,00,000 pay zero income tax. With the ₹75,000 standard deduction for salaried employees, individuals with gross salary up to ₹12,75,000 effectively pay no income tax under the New Regime.

2. Revised New Tax Regime Slabs (FY 2025-26) The New Tax Regime now has seven slabs:

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4,00,000 | 0% (Nil) |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

3. Standard Deduction Increased to ₹75,000 The standard deduction for salaried individuals and pensioners has been raised to ₹75,000 under the New Tax Regime (it was ₹50,000 under the Old Regime, which remains unchanged).

4. TDS on Rent Threshold Raised The TDS deduction limit on rental income has been raised to ₹50,000 per month (from ₹40,000), reducing compliance burden for landlords and tenants.

5. Senior Citizen Interest Deduction Doubled The deduction limit for senior citizens on interest income (Section 80TTB) has been increased from ₹50,000 to ₹1,00,000 per year.

6. New Tax Regime is Now the Default Unless you explicitly opt for the Old Tax Regime while filing your ITR (or inform your employer at the start of the financial year), the New Tax Regime will apply by default from FY 2023-24 onwards.

How to Use the Click2Calculate India Income Tax Calculator

Step 1 — Select the Financial Year Choose FY 2025-26 (AY 2026-27) for current year tax calculation. The calculator is updated to reflect Union Budget 2025 changes.

Step 2 — Select Your Age Group Your age determines which tax slab applies under the Old Regime:

- General individuals (below 60 years)

- Senior Citizens (60–80 years) — basic exemption limit ₹3,00,000 under Old Regime

- Super Senior Citizens (above 80 years) — basic exemption limit ₹5,00,000 under Old Regime

Age has no differential impact under the New Tax Regime.

Step 3 — Enter Your Income Details

- Gross Salary / CTC (Cost to Company)

- Basic Salary (used for HRA and PF calculation)

- House Rent Allowance (HRA) received

- Actual Rent Paid per month

- City type (Metro / Non-metro — affects HRA exemption)

- Other income: interest income, rental income, capital gains, freelance income

Step 4 — Enter Deductions (Old Regime) If comparing under the Old Tax Regime, enter:

- Section 80C investments (EPF, PPF, ELSS, LIC premium, tuition fees, home loan principal — up to ₹1,50,000)

- Section 80D (health insurance premium — up to ₹25,000; ₹50,000 for senior citizens)

- Section 80CCD(1B) — additional NPS contribution (up to ₹50,000)

- Section 24(b) — home loan interest for self-occupied property (up to ₹2,00,000)

- Section 80E — education loan interest (no upper limit)

- Section 80G — donations to approved charities (50% or 100% deductible depending on institution)

- Section 80TTA — savings account interest (up to ₹10,000; ₹50,000 for senior citizens under 80TTB)

Step 5 — Select Regime and Click Calculate Choose New Regime or Old Regime (or let the calculator compare both automatically). Results show:

- Gross taxable income

- Total exemptions and deductions

- Net taxable income

- Income tax on each slab

- Surcharge (if applicable)

- Health and Education Cess (4% on tax + surcharge)

- Total tax payable

- Monthly TDS amount

- Estimated take-home (in-hand) salary per month

Old Tax Regime vs New Tax Regime: Complete Comparison

This is the single most important financial decision for every salaried Indian taxpayer. Here is a definitive comparison:

| Parameter | Old Tax Regime | New Tax Regime |

|---|---|---|

| Basic Exemption | ₹2,50,000 | ₹4,00,000 |

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 87A Rebate | Up to ₹12,500 (income ≤ ₹5L) | Up to ₹60,000 (income ≤ ₹12L) |

| HRA Exemption | Available | Not Available |

| LTA Exemption | Available | Not Available |

| Section 80C | Up to ₹1,50,000 | Not Available |

| Section 80D | Up to ₹25,000 / ₹50,000 | Not Available |

| Home Loan Interest (Sec 24b) | Up to ₹2,00,000 (self-occ) | Not Available |

| NPS Employer Contribution 80CCD(2) | Available | Available (up to 14% of salary) |

| Default Regime (FY 2025-26) | No (must opt-in) | Yes |

| Switch Flexibility | Every year (salaried) | Every year (salaried) |

| Top Slab Rate | 30% (above ₹10L) | 30% (above ₹24L) |

| Best For | High deductions (>₹3.75L) | Low deductions or beginners |

When the Old Regime Wins: The Old Regime is more beneficial when your total eligible deductions and exemptions exceed approximately ₹3.75 lakh per year. This typically means: you pay significant rent (high HRA exemption), invest ₹1.5 lakh in 80C instruments, pay health insurance premiums, AND have a home loan with interest payments exceeding ₹1.5 lakh per year.

When the New Regime Wins: For most salaried individuals — especially those earning under ₹12.75 lakh, those without major deductions, or those just starting their career — the New Regime results in zero or lower tax with no investment obligations. At most income levels above ₹15 lakh, a detailed calculation (which our calculator performs instantly) is needed to determine the better option.

Income Tax Calculation Examples for FY 2025-26

Example 1: ₹8 Lakh Annual Salary (Young Professional)

New Tax Regime:

- Gross Salary: ₹8,00,000

- Less Standard Deduction: ₹75,000

- Net Taxable Income: ₹7,25,000

- Tax on ₹7,25,000: ₹4L–₹8L @ 5% = ₹16,250 on ₹3,25,000 = ₹16,250

- Section 87A Rebate: ₹16,250 (full rebate since income ≤ ₹12L)

- Total Tax Payable: ₹0

- Monthly Take-Home: ~₹66,667

Old Tax Regime (with ₹1.5L in 80C + ₹25K in 80D + ₹50K Standard Deduction):

- Taxable Income: ₹8L – ₹50K – ₹1.5L – ₹25K = ₹5,75,000

- Tax: ₹2.5L–₹5L @ 5% = ₹12,500; ₹5L–₹5.75L @ 20% = ₹15,000 → ₹27,500

- Section 87A Rebate: ₹12,500

- Tax after rebate: ₹15,000 + 4% Cess = ₹15,600

- New Regime is better for this income level

Example 2: ₹15 Lakh Annual Salary (Mid-Level Professional)

New Tax Regime:

- Gross Salary: ₹15,00,000

- Less Standard Deduction: ₹75,000

- Taxable Income: ₹14,25,000

- Tax Calculation:

- 0 on first ₹4L = ₹0

- 5% on ₹4L–₹8L = ₹20,000

- 10% on ₹8L–₹12L = ₹40,000

- 15% on ₹12L–₹14.25L = ₹33,750

- Total Tax: ₹93,750

- Add 4% Cess: ₹3,750

- Total Tax: ₹97,500 | Monthly TDS: ~₹8,125

Old Tax Regime (with ₹50K Standard + ₹1.5L 80C + ₹25K 80D + ₹2L Home Loan Interest):

- Taxable Income: ₹15L – ₹50K – ₹1.5L – ₹25K – ₹2L = ₹10,75,000

- Tax: ₹2.5L–₹5L @ 5% = ₹12,500; ₹5L–₹10L @ 20% = ₹1,00,000; ₹10L–₹10.75L @ 30% = ₹22,500 → ₹1,35,000

- Add 4% Cess: ₹5,400

- Total Tax: ₹1,40,400 | Old Regime costs MORE by ~₹42,900

- New Regime wins in this scenario

Example 3: ₹25 Lakh Annual Salary (Senior Manager — High Deductions)

New Tax Regime:

- Taxable Income after ₹75K standard deduction: ₹24,25,000

- Tax: ₹93,750 (on first ₹24L) + 30% on ₹25K = ₹7,500 → ₹1,01,250… (calculated accurately by the tool)

- Approximate Total Tax (with 4% cess): ~₹3,82,200

Old Tax Regime (with ₹50K Standard + ₹1.5L 80C + ₹50K NPS 80CCD(1B) + ₹25K 80D + ₹2L Home Loan + ₹4L HRA Exemption):

- Taxable Income: ₹25L – ₹50K – ₹1.5L – ₹50K – ₹25K – ₹2L – ₹4L = ₹16,25,000

- Approximate Total Tax (with cess): ~₹3,34,750

- Old Regime saves ~₹47,450 in this high-deduction scenario

For accurate, personalised calculation at any income level, use the Click2Calculate Salary Income Tax Calculator.

Income Tax Slabs Under Old Regime FY 2025-26 (AY 2026-27)

The Old Tax Regime slabs have remained unchanged for several years:

For Individuals Below 60 Years:

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

For Senior Citizens (60–80 Years):

| Income Slab | Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

For Super Senior Citizens (Above 80 Years):

| Income Slab | Tax Rate |

|---|---|

| Up to ₹5,00,000 | Nil |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Surcharge Rates (Both Regimes, FY 2025-26):

| Total Income | Surcharge Rate |

|---|---|

| ₹50 lakh to ₹1 crore | 10% |

| ₹1 crore to ₹2 crore | 15% |

| ₹2 crore to ₹5 crore | 25% (capped at 25% under New Regime) |

| Above ₹5 crore | 37% (Old Regime) / 25% (New Regime) |

Health and Education Cess: 4% is added on (income tax + surcharge) under both regimes.

How to Calculate HRA Exemption Using Our Calculator

House Rent Allowance (HRA) is one of the largest and most commonly used exemptions available under the Old Tax Regime. It is not available under the New Tax Regime.

HRA Exemption = Least of the Following Three:

- Actual HRA received from employer

- Actual rent paid minus 10% of Basic Salary + DA

- 50% of (Basic Salary + DA) for metro cities OR 40% for non-metro cities

Metro cities for HRA: Mumbai, Delhi, Kolkata, Chennai

HRA Calculation Example:

- Basic Salary: ₹6,00,000 per year

- HRA Received: ₹3,00,000 per year

- Actual Rent Paid: ₹24,000 per month = ₹2,88,000 per year

- City: Bengaluru (Non-metro)

Exemption = Least of:

- ₹3,00,000 (actual HRA received)

- ₹2,88,000 – 10% × ₹6,00,000 = ₹2,88,000 – ₹60,000 = ₹2,28,000

- 40% × ₹6,00,000 = ₹2,40,000

HRA Exemption = ₹2,28,000 (the lowest of the three)

Enter these values in the Click2Calculate HRA calculator tab to get your exempt amount instantly — no manual computation needed.

CTC vs Gross Salary vs Take-Home Salary: What Each Means

Many salaried employees confuse CTC (Cost to Company), Gross Salary, and Take-Home (Net) Salary. Here is the exact breakdown:

CTC (Cost to Company) The total annual cost your employer incurs to employ you. Includes:

- Basic Salary

- HRA, DA, and other allowances

- Employer’s contribution to EPF (12% of Basic)

- Employer’s contribution to NPS (if applicable)

- Medical reimbursement, meal vouchers, Leave Travel Allowance

- Gratuity provision (4.81% of Basic)

- Any other perquisites

Gross Salary CTC minus employer’s contributions (EPF, NPS, Gratuity). This is what appears on your salary slip before deductions.

Net / Take-Home Salary Gross Salary minus:

- Employee’s EPF contribution (12% of Basic)

- Professional Tax (state-dependent, max ₹2,500/year)

- Income Tax (TDS deducted monthly by employer)

- Any other deductions (health insurance premium deducted by employer, etc.)

Example:

| Component | Amount |

|---|---|

| CTC | ₹12,00,000 |

| Less: Employer’s EPF | ₹57,600 |

| Less: Employer’s Gratuity Provision | ₹27,720 |

| Gross Salary | ₹11,14,680 |

| Less: Employee’s EPF | ₹57,600 |

| Less: Professional Tax | ₹2,400 |

| Less: Income Tax (TDS) | ₹0 (income ≤ ₹12.75L under New Regime) |

| Monthly Take-Home | ~₹87,890 |

Use the Click2Calculate CTC to take-home salary calculator to break down any CTC offer into its components and find your actual in-hand monthly salary.

Key Tax-Saving Deductions Under the Old Tax Regime

If you are considering the Old Tax Regime, understanding all available deductions is critical to reducing your tax liability:

Section 80C (Limit: ₹1,50,000) The most widely used deduction. Eligible instruments:

- Employee Provident Fund (EPF) — employer deducts automatically

- Public Provident Fund (PPF)

- Equity Linked Savings Scheme (ELSS) mutual funds

- National Savings Certificate (NSC)

- 5-year Tax-Saving Fixed Deposits

- Life Insurance Premiums (LIC or any insurer)

- Home Loan Principal Repayment

- Sukanya Samriddhi Yojana (SSY) — girl child savings scheme

- Senior Citizens Savings Scheme (SCSS)

- Tuition fees for up to 2 children

Section 80CCD(1B) — Additional NPS (Limit: ₹50,000) An additional deduction of up to ₹50,000 for contributions to the National Pension System (NPS Tier 1 account). This is over and above the ₹1.5 lakh 80C limit — meaning a total of ₹2 lakh can be claimed for these two sections combined.

Section 80D — Health Insurance (Limit: ₹25,000 / ₹50,000 / ₹75,000)

- Self, spouse, and children: up to ₹25,000 (₹50,000 if insured is senior citizen)

- Parents: additional ₹25,000 (₹50,000 if parents are senior citizens)

- Maximum combined: ₹1,00,000 (if both self and parents are senior citizens)

Section 24(b) — Home Loan Interest (Limit: ₹2,00,000 for self-occupied) Interest paid on a home loan for your self-occupied property is deductible up to ₹2,00,000 per year. For let-out property, the entire interest is deductible (no upper limit), though losses can only be set off up to ₹2L against other income.

Section 80E — Education Loan Interest (No Limit) Interest paid on a loan taken for higher education (self, spouse, children, or a student for whom you are the legal guardian) is fully deductible. No upper cap. Applicable for 8 consecutive years starting from when you begin repaying the loan.

Section 80G — Charitable Donations (50% or 100%) Donations to approved funds and charitable institutions qualify for 50% or 100% deduction. Notable 100% deductions include the PM Relief Fund, National Defence Fund, and PMNRF. Most other charitable trusts qualify for 50% deduction.

Section 80TTA / 80TTB — Savings Interest

- Section 80TTA: Interest earned on savings bank accounts — deduction up to ₹10,000 (for non-senior citizens)

- Section 80TTB: For senior citizens — interest on savings, FDs, recurring deposits — deduction up to ₹1,00,000 (from FY 2025-26)

Section 80GG — Rent Deduction (No HRA in salary) For individuals who pay rent but do not receive HRA as part of their salary. Deduction is the least of:

- Rent paid minus 10% of total income

- 25% of total income

- ₹5,000 per month (₹60,000 per year)

Global Income Tax Calculator: Calculate Salary After Tax in 10+ Countries

One of the defining features of Click2Calculate is its global income tax calculator — covering salary tax systems across the world’s major economies. This tool is invaluable for:

- Expats and international professionals comparing job offers across countries

- Digital nomads choosing a tax-friendly base country

- HR and Finance teams calculating employment costs for global hiring

- Students and graduates deciding which country to work in first

- NRIs comparing their India tax obligations against their country of residence

United States — Federal Income Tax + Social Security + Medicare

The US uses a progressive federal income tax with seven brackets for the 2025 tax year (filing in 2026):

| Income (Single Filer) | Federal Tax Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 – $48,475 | 12% |

| $48,476 – $103,350 | 22% |

| $103,351 – $197,300 | 24% |

| $197,301 – $250,525 | 32% |

| $250,526 – $626,350 | 35% |

| Above $626,350 | 37% |

FICA (Social Security + Medicare):

- Social Security: 6.2% on wages up to $176,100

- Medicare: 1.45% on all wages (+ additional 0.9% above $200K)

State Income Tax: Varies by state. States like Texas, Florida, Washington, and Nevada have no state income tax. California tops the list at 13.3% for high earners.

Standard Deduction (2025): $14,600 (Single) | $29,200 (Married Filing Jointly)

The Click2Calculate US salary tax calculator accounts for federal tax, Social Security, Medicare, and lets you select your state to include state income tax.

United Kingdom — Income Tax + National Insurance (2025-26)

The UK tax year runs from 6 April to 5 April. For the 2025-26 tax year:

Income Tax Bands (England, Wales, Northern Ireland):

| Band | Income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Above £125,140 | 45% |

National Insurance (Employee):

- 8% on earnings between £12,570–£50,270 per year

- 2% on earnings above £50,270

Example: A £50,000 annual salary in the UK yields approximately £37,200 in take-home pay after income tax and National Insurance — an effective total deduction rate of about 25.6%.

Australia — ATO Income Tax + Medicare Levy (FY 2025-26)

Australia’s financial year runs July 1 to June 30. For FY 2025-26:

Resident Individual Tax Brackets:

| Income | Tax Rate |

|---|---|

| $0 – $18,200 | 0% (Tax-Free Threshold) |

| $18,201 – $45,000 | 16% |

| $45,001 – $135,000 | 30% |

| $135,001 – $190,000 | 37% |

| Above $190,000 | 45% |

Medicare Levy: 2% of taxable income (most residents) Low Income Tax Offset (LITO): Up to $700 offset for lower-income earners

Australia has no state income tax (unlike the US and Canada) — making the calculation simpler. From 1 July 2026, the 16% bracket drops to 15%.

Example: An A$80,000 salary yields approximately A$61,832 after tax and Medicare levy — an effective rate of about 22.7%.

Canada — Federal + Provincial Income Tax (2025)

Canada has a combined federal + provincial tax system. Federal brackets for 2025:

| Income | Federal Rate |

|---|---|

| Up to C$57,375 | 15% |

| C$57,376 – C$114,750 | 20.5% |

| C$114,751 – C$158,519 | 26% |

| C$158,520 – C$220,000 | 29% |

| Above C$220,000 | 33% |

Provincial tax ranges from 4% to 25.75% depending on province. Ontario adds 5.05%–13.16%; British Columbia 5.06%–20.5%; Alberta 10% flat rate.

CPP (Canada Pension Plan): 5.95% on earnings between C$3,500 and C$68,500 EI (Employment Insurance): 1.66% on insurable earnings up to C$63,200

Germany — Income Tax + Solidarity Surcharge + Social Contributions (2025)

Germany has one of the highest effective total tax burdens in the world due to mandatory social contributions:

- Income Tax: Progressive from 14% to 45%

- Solidarity Surcharge: 5.5% on income tax (only for higher earners post-2021 reforms)

- Kirchensteuer (Church Tax): 8–9% of income tax (only if registered with a religious body — opt-out available)

- Health Insurance (Gesetzliche Krankenversicherung): ~7.3% employee contribution

- Pension Insurance (Rentenversicherung): 9.3% employee contribution

- Unemployment Insurance: 1.3% employee contribution

- Long-term Care Insurance: ~1.8% employee contribution

Total deductions from gross salary in Germany typically range from 35% to 45% for average earners.

UAE & Singapore — Zero Income Tax Jurisdictions

The United Arab Emirates and Singapore are among the world’s most attractive destinations for international professionals:

- UAE: No personal income tax whatsoever. Gross salary = net salary for employees. (Note: Corporate tax of 9% on business profits was introduced from June 2023 for businesses above AED 375,000 profit — does not affect employee salaries.)

- Singapore: Progressive income tax from 0% to 24% for residents. For a S$100,000 salary, effective tax rate is approximately 7–8%. No capital gains tax, no inheritance tax.

These zero or low-tax environments are a major reason why Dubai and Singapore attract significant international talent migration and are heavily searched for salary comparison.

Country-by-Country Salary After Tax Comparison

The table below shows approximate annual take-home pay on a standardised gross salary of USD $80,000 across major economies (2025-26, single employee, no dependents, no special deductions):

| Country | Gross (USD equiv.) | Est. Income Tax + Social | Take-Home (USD equiv.) | Effective Rate |

|---|---|---|---|---|

| UAE | $80,000 | $0 | $80,000 | 0% |

| Singapore | $80,000 | ~$5,500 | ~$74,500 | ~6.9% |

| USA (Texas, no state tax) | $80,000 | ~$16,800 | ~$63,200 | ~21% |

| Australia | $80,000 | ~$19,500 | ~$60,500 | ~24.4% |

| Canada (Ontario) | $80,000 | ~$24,000 | ~$56,000 | ~30% |

| UK | $80,000 | ~$22,500 | ~$57,500 | ~28.1% |

| India (₹67L equiv., New Regime) | $80,000 | ~$14,200 | ~$65,800 | ~17.8% |

| Germany | $80,000 | ~$32,000 | ~$48,000 | ~40% |

Values are approximations for illustration. Use the Click2Calculate global salary tax calculator for exact results based on actual exchange rates and current tax rules.

Who Should Use This Salary & Income Tax Calculator?

Salaried Professionals (India)

Verify your employer’s TDS deduction is correct. Calculate whether the New or Old Regime is better for your specific income and deduction profile. Understand your actual in-hand salary after all deductions.

Job Seekers and Career Changers

Evaluate a new job offer: convert CTC to actual take-home. Compare two competing offers with different salary structures (one with higher HRA, one with higher Basic). Understand the real financial difference.

NRIs (Non-Resident Indians)

NRIs are taxed in India only on income earned or accrued in India. Interest on NRO accounts is taxable; interest on NRE accounts is not. Understanding India’s tax liability alongside the tax obligations in your country of residence is critical — and our dual-country comparison tool helps.

Freelancers and Self-Employed Professionals

Income tax for freelancers is calculated differently — income from freelancing is treated as “Profits and Gains from Business or Profession.” Advance tax payment in quarterly instalments is mandatory when annual tax liability exceeds ₹10,000. Use the calculator to estimate your quarterly advance tax instalments.

Expats and Digital Nomads

Comparing take-home salary across countries before accepting an international posting or choosing where to base yourself. Our global income tax comparison shows real after-tax salary across 10+ countries in a single view.

HR, Finance, and Payroll Teams

Estimating TDS to be deducted and deposited for employees. Structuring salary packages tax-efficiently (optimal split between Basic, HRA, Special Allowance, and perquisites). Managing compliance with Form 16 and quarterly TDS returns.

Retirees and Senior Citizens

Senior citizens have different tax slabs under the Old Regime (₹3L exemption vs ₹2.5L for others) and higher deductions available under 80TTB. The calculator applies these automatically when you select Senior Citizen age bracket.

Income Tax Filing: Key Dates and Documents You Need

Important Dates for FY 2025-26 (AY 2026-27)

| Event | Date |

|---|---|

| Start of Financial Year | 1 April 2025 |

| End of Financial Year | 31 March 2026 |

| Advance Tax (Q1) | 15 June 2025 |

| Advance Tax (Q2) | 15 September 2025 |

| Advance Tax (Q3) | 15 December 2025 |

| Advance Tax (Q4) | 15 March 2026 |

| Form 16 from Employer | By 15 June 2026 |

| ITR Filing Deadline (Non-Audit) | 31 July 2026 |

| ITR Filing Deadline (Audit cases) | 31 October 2026 |

| Belated ITR Deadline | 31 December 2026 |

Documents Required for ITR Filing

- Form 16 — Issued by your employer showing salary paid and TDS deducted

- Form 26AS — Tax credit statement from the Income Tax Department (available on e-filing portal)

- Annual Information Statement (AIS) — Comprehensive income information from various sources

- Bank Statements — For interest income and other credits

- Investment Proofs — For 80C, 80D, NPS, donations

- Rent Receipts — For claiming HRA exemption

- Home Loan Statement — For Section 24(b) and 80C (principal repayment) claims

- Capital Gains Statements — From brokers/mutual fund houses for equity, debt fund, or property transactions

Income Tax Calculator FAQs — Most Searched Questions Answered

Is income up to ₹12 lakh completely tax-free in FY 2025-26? Yes, under the New Tax Regime for FY 2025-26, individuals with total income up to ₹12,00,000 are eligible for a full tax rebate under Section 87A (₹60,000 rebate). For salaried employees, the ₹75,000 standard deduction means gross salary up to ₹12,75,000 results in zero tax liability. However, special-rate incomes like capital gains are excluded from this rebate.

Which is better — old or new tax regime for ₹10 lakh salary? At ₹10 lakh salary with minimal deductions, the New Regime is almost always better. With the standard deduction of ₹75,000, your taxable income under the New Regime is ₹9,25,000, resulting in tax of approximately ₹42,500 + cess. Under the Old Regime with ₹1.5L in 80C and ₹25K in 80D, taxable income is ₹7,75,000 and tax is around ₹75,000 + cess. Use the calculator for your exact deduction profile.

Which is better — old or new tax regime for ₹15 lakh salary? Typically the New Regime produces lower tax for a ₹15 lakh salary unless you have combined deductions (HRA + 80C + 80D + Home Loan Interest) exceeding approximately ₹3.75–4 lakh. Run your actual figures through the calculator for a definitive answer.

What is the income tax on ₹20 lakh salary under the New Regime? Under the New Tax Regime for FY 2025-26: Taxable Income after ₹75K standard deduction = ₹19,25,000. Approximate tax: ₹0 + ₹20,000 + ₹40,000 + ₹60,000 + ₹48,750 = ₹1,68,750 + 4% cess = approximately ₹1,75,500. Monthly TDS would be approximately ₹14,625.

What is the last date to file income tax return for FY 2025-26? The deadline to file your ITR for FY 2025-26 (AY 2026-27) is 31 July 2026 for non-audit cases. For taxpayers requiring audit, it is 31 October 2026. Belated returns can be filed until 31 December 2026 with a late filing fee of ₹5,000 (₹1,000 if income is below ₹5 lakh).

Can I switch between old and new tax regime every year? Yes — salaried employees can switch between the Old and New Tax Regimes every financial year. You inform your employer at the start of the year for TDS purposes. When filing ITR, you can again choose the most beneficial regime. Business owners, however, can switch only once from New to Old Regime and back only once.

What is the standard deduction for FY 2025-26? ₹75,000 under the New Tax Regime and ₹50,000 under the Old Tax Regime. This flat deduction is available to all salaried individuals and pensioners without needing to submit any proof or bills.

How is TDS calculated on salary? Your employer estimates your total annual income, subtracts eligible deductions and the standard deduction, calculates your annual tax liability, and divides it by 12 to arrive at monthly TDS. If you do not submit proof of investments and deductions to your employer, TDS may be deducted at a higher rate.

Is professional tax deductible from income tax? Yes, professional tax (a state-level tax, maximum ₹2,500/year) paid is deductible from salary income before calculating income tax. It is separately deducted under Section 16(iii) of the Income Tax Act.

How do I calculate advance tax? If your estimated tax liability for the year exceeds ₹10,000, you must pay advance tax in four instalments: 15% by 15 June, 45% by 15 September, 75% by 15 December, and 100% by 15 March of the financial year. Failure to pay advance tax on time attracts interest under Sections 234B and 234C.

What is Form 16 and why is it important? Form 16 is a TDS certificate issued by your employer by 15 June each year. It certifies the salary paid to you and the tax deducted at source during the financial year. It is the primary document used to file your ITR and consists of two parts: Part A (TDS details, employer and employee PAN) and Part B (salary breakup, deductions, and tax computation).

How is income tax calculated for a salary of ₹50 lakh? At ₹50 lakh under the New Tax Regime: Taxable income after ₹75K standard deduction = ₹49,25,000. Tax on this includes the 30% rate on income above ₹24L, plus a 10% surcharge (since income exceeds ₹50L), plus 4% cess. The Click2Calculate income tax calculator handles all these steps including marginal relief — enter your income for an exact result.

Tax Saving Strategies: Legally Reduce Your Income Tax Liability

Knowing your tax liability is the first step. Reducing it legally is the second. Here are the most effective tax-saving strategies for FY 2025-26:

For New Regime Taxpayers

Under the New Regime, deductions are limited, but these remain available:

- Section 80CCD(2): Employer’s contribution to NPS up to 14% of salary is deductible — a significant benefit if your employer offers NPS. Request your HR to structure your CTC to maximise this.

- Standard Deduction: Automatically applied. No action needed.

- Family Pension Deduction: One-third of family pension (or ₹25,000, whichever is lower) is deductible.

- No tax up to ₹12L: Ensure you are aware of this — many taxpayers unnecessarily file using the Old Regime and pay more tax.

For Old Regime Taxpayers

- Maximise Section 80C: Invest ₹1.5L across EPF (auto-deducted), PPF, ELSS, and LIC to claim full ₹1.5L deduction.

- Add NPS under 80CCD(1B): Additional ₹50,000 deduction for NPS contributions — reduces taxable income by ₹2L in total when combined with 80C.

- Buy health insurance: Section 80D deduction for your family and parents. Premium for senior citizen parents yields ₹50K extra deduction.

- Claim HRA fully: Maintain rent receipts, rental agreement, and landlord’s PAN (for rent above ₹1L/year). Ensure your HRA component and rent paid are structured optimally.

- Education loan interest (80E): If you are repaying a student loan, the full interest component is deductible for up to 8 years.

- Timing capital gains: Consider booking long-term capital gains (LTCG) up to ₹1.25 lakh per year tax-free under Section 112A before the financial year ends.

Why Use Click2Calculate’s Salary & Income Tax Calculator?

There are dozens of income tax calculators online — from the official Income Tax Department portal to private tools by Groww, ClearTax, PolicyBazaar, and banking websites. Here is what makes Click2Calculate different:

One tool, multiple countries. Most Indian calculators cover only India. Click2Calculate’s global salary tax calculator covers India, USA, UK, Australia, Canada, Germany, UAE, Singapore, and more — all in one place.

Side-by-side regime comparison. Enter your details once and instantly see your tax under both Old and New Tax Regimes, which regime is better, and by exactly how much.

CTC to take-home breakdown. Not just income tax — the calculator shows your complete salary structure: CTC → Gross Salary → Deductions (EPF, PT, TDS) → Net Take-Home, with monthly and annual figures.

HRA calculator integrated. Calculate your HRA exemption using the three-condition formula without switching tools.

No registration required. Free to use, no login, no data storage. Results are instant and private.

Updated for latest budget. Always current with the most recent Finance Act provisions, tax slabs, and budget announcements.

Related Calculators on Click2Calculate

Complete your financial planning with these companion tools:

- HRA Calculator — Calculate HRA exemption under the three-condition rule for metro and non-metro cities

- Take-Home Salary Calculator — CTC to in-hand salary breakdown with EPF, PT, and TDS

- Advance Tax Calculator — Estimate quarterly advance tax instalments (15/45/75/100% rule)

- 80C Investment Calculator — Plan and optimise ₹1.5 lakh investment across PPF, ELSS, EPF, NSC

- NPS Calculator — Calculate pension corpus and tax savings under Section 80CCD

- SIP Calculator — Plan ELSS mutual fund SIP investments for dual benefit of wealth creation + 80C deduction

- EMI Calculator — Calculate home loan EMI and interest component (relevant for Section 24(b) planning)

- Gratuity Calculator — Estimate gratuity entitlement and its tax treatment

- Global Salary Comparison Tool — Compare gross vs net salary across 10+ countries at a single income level

Disclaimer: All income tax calculations, examples, and estimates on this page are for informational and planning purposes only. Tax rules, slabs, deductions, and rebates are subject to change through Union Budgets and Finance Acts. Actual tax liability may differ based on individual circumstances, additional sources of income, specific deduction eligibility, and applicable surcharges. This content is current as of June 2026 and reflects provisions of the Finance Act 2025 for FY 2025-26 (AY 2026-27). For personalised tax advice and ITR filing assistance, consult a qualified Chartered Accountant or SEBI/CBDT-registered tax professional. For global tax data, consult the relevant country’s official tax authority (IRS for USA, HMRC for UK, ATO for Australia, CRA for Canada).

Last Updated: June 2026

{kind=link}